Post Office FD Fixed Deposit Scheme : ₹2 Lakh Investment Returns in 2 Years

In India, small savings schemes have always played a vital role in the financial planning of millions of households. Among these, the Post Office Fixed Deposit (FD) Scheme, also known as the National Savings Time Deposit Account (TD), is one of the most popular and trusted savings instruments. Operated by the Department of Posts under the Government of India, it provides guaranteed returns with government backing, making it one of the safest options for conservative investors.

Many individuals often wonder: If I invest ₹2,00,000 in a Post Office FD for 2 years, how much money will I get back? This article gives you a comprehensive 4000-word guide on how the scheme works, the interest calculation, expected maturity value, and why it might (or might not) be the right option for you.

What is Post Office FD (Time Deposit)?

The Post Office FD scheme is very similar to a bank fixed deposit. You deposit a lump sum amount for a fixed tenure, and the government pays you a predetermined interest rate. At the end of the tenure, you receive your principal amount plus the accumulated interest.

Key features include:

- Available for 1 year, 2 years, 3 years, and 5 years.

- Interest rates are revised every quarter by the Ministry of Finance.

- Minimum deposit: ₹1,000.

- No maximum limit.

- Interest is compounded quarterly but payable annually.

- Safe and fully backed by the Government of India.

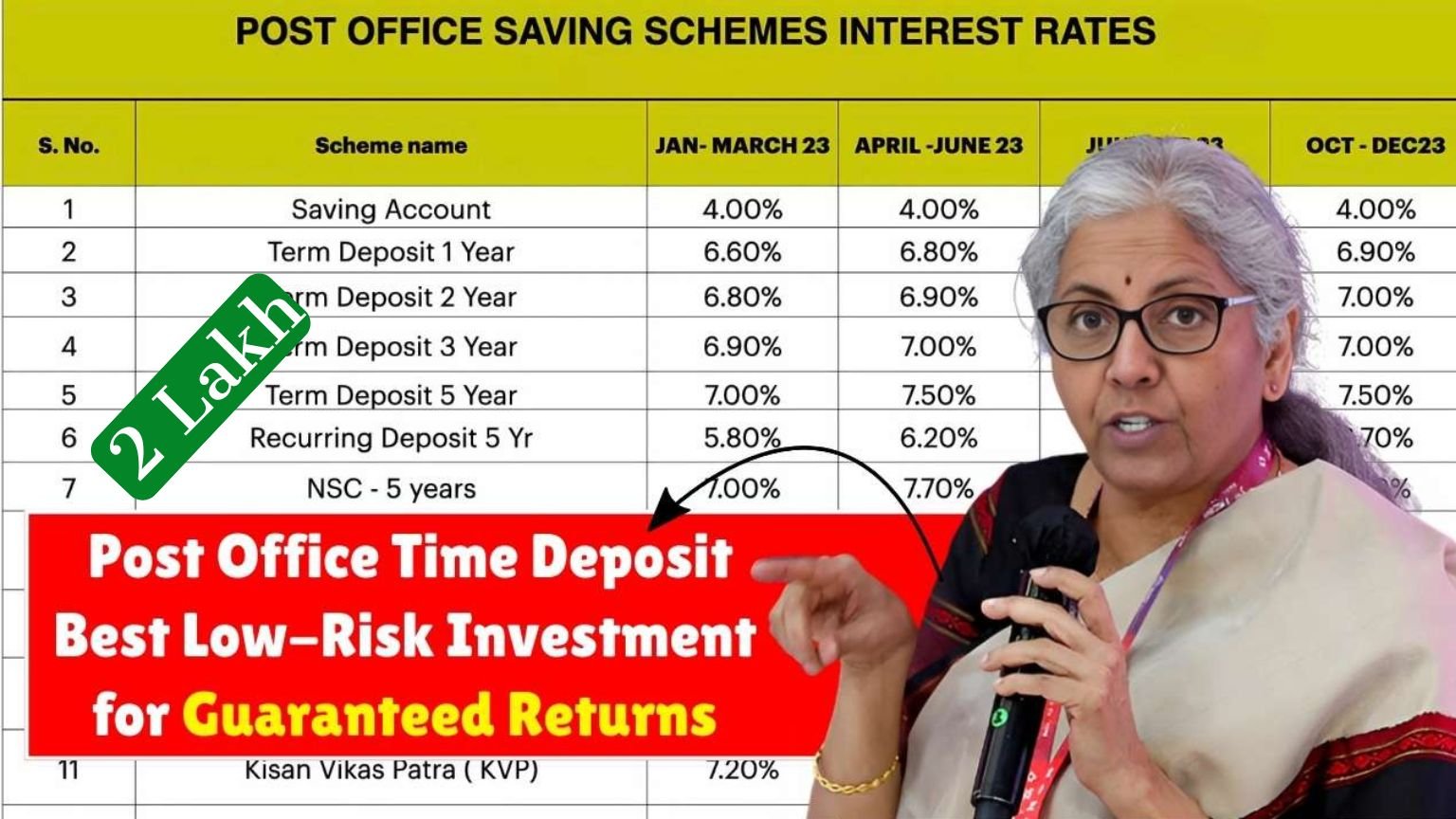

Current Interest Rates (As of 2025)

The interest rates of Post Office FD (Time Deposit) for October–December 2025 quarter are as follows:

- 1 year – 6.9% per annum

- 2 years – 7.0% per annum

- 3 years – 7.1% per annum

- 5 years – 7.5% per annum (eligible for tax deduction under Section 80C)

For our calculation, we will use the 2-year FD rate of 7.0% per annum.

Example: ₹2 Lakh Investment for 2 Years

Let’s calculate the maturity value if someone invests ₹2,00,000 for 2 years in a Post Office FD.

- Principal (P) = ₹2,00,000

- Rate of Interest (R) = 7.0% per annum

- Time (T) = 2 years

- Compounding = Quarterly

Step-by-Step Breakdown of Returns

Year 1:

- Initial Deposit: ₹2,00,000

- Interest earned in first year ≈ ₹14,700

Year 2:

- New principal = ₹2,14,700

- Interest earned in second year ≈ ₹14,900

Final Maturity = ₹2,29,600

Benefits of Post Office FD

- Government-backed safety – No risk of default.

- Flexible tenure – 1, 2, 3, or 5 years.

- Decent returns – Competitive interest compared to bank FDs.

- Tax benefits – 5-year FD eligible under Section 80C.

- Transfer facility – Can transfer FD from one post office to another.

- Nomination facility – Available.

- Premature withdrawal – Allowed after 6 months (with penalty).

Comparison: Post Office FD vs Bank FD

| Feature | Post Office FD | Bank FD |

|---|---|---|

| Safety | 100% Govt-backed | Depends on bank; insured up to ₹5 lakh |

| Tenure | 1 to 5 years | 7 days to 10 years |

| Interest Rate | 6.9%–7.5% | 5%–7.25% (varies by bank) |

| Tax Benefit | Only 5-year FD under Sec 80C | Only 5-year FD under Sec 80C |

| Compounding | Quarterly | Quarterly/Monthly/Annually |

Taxation on FD Returns

- Interest earned on Post Office FD is fully taxable as per your income tax slab.

- No TDS is deducted at source, but you must declare it while filing ITR.

- 5-year FD offers tax deduction (Sec 80C) up to ₹1.5 lakh investment per year.

Who Should Invest in Post Office FD?

- Retired individuals looking for guaranteed safe returns.

- Conservative investors who do not want market risk.

- Rural citizens who prefer Post Office over banks.

- Parents investing for children’s short-term goals.

Step-by-Step Process to Open a Post Office FD

- Visit your nearest Post Office.

- Fill the Post Office Time Deposit application form.

- Submit KYC documents (Aadhaar, PAN, Address proof, Photograph).

- Deposit cash/cheque or transfer from your Post Office savings account.

- Collect the FD certificate as proof of investment.

Online Access

- If you have a Post Office Savings Account with internet banking, you can open and manage FD online.

- India Post Payment Bank (IPPB) app also supports linked services.

Drawbacks of Post Office FD

- No loan facility against FD.

- Interest is taxable.

- Limited tenure options (only 1, 2, 3, 5 years).

- Slightly less flexible compared to banks/NBFCs.

Alternative Investment Options

If you are considering short-term investments like a 2-year FD, you can also look at:

- Bank FDs (for liquidity and different tenures).

- Recurring Deposit (RD) in Post Office.

- National Savings Certificate (NSC) – 5 years.

- Senior Citizen Savings Scheme (SCSS) (if age > 60).

- Kisan Vikas Patra (KVP) – doubles money in ~115 months.

Here’s what I found about the link / method to apply online for Post Office Fixed Deposit (Time Deposit) in India, and steps:

Link / Portal to apply

- The India Post Net Banking / e-banking portal is one primary route. (You can access India Post’s net banking services via their site) (India Post)

- Under the “Internet Banking” / “General Services / Service Request” section, there is an option to open a new Time Deposit (FD) / TD (Term Deposit) account. (India Post)

- Some guides say you can go via the India Post eBanking website (ebanking.indiapost.gov.in) → login → “Service Request” → “New Request” → choose “Fixed Deposit / Time Deposit” to apply online.

Here are several Post Office / Small Savings schemes in India (beyond just Fixed Deposits), with their features, pros/cons, and how they work. (This is ~2,000 words, so you can get a good overview.)

Overview of Post Office / Small Savings Schemes

The Indian Post Office (through the Department of Posts) runs a number of small savings / investment schemes which are considered safe (backed by government) and are widely used by common people. These schemes suit different investment horizons, goals, and liquidity preferences.

Typical schemes include:

- Post Office Savings Account

- Recurring Deposit (RD) / National Savings RD

- Monthly Income Scheme (MIS) / POMIS

- Time Deposit / Term Deposit (1, 2, 3, 5 years)

- National Savings Certificate (NSC)

- Public Provident Fund (PPF)

- Sukanya Samriddhi Yojana (for girl children)

- Senior Citizens Savings Scheme (SCSS)

- Kisan Vikas Patra (KVP)

- Mahila Samman Savings Certificate

In the next sections, I’ll explain each, how they work, interest rate behavior, advantages, and typical use-cases.

Post Office Savings Account

What it is

This is like a regular “savings bank account” but held in the post office. Anyone (adult, minor) can open one.

Key features

- Interest rate: ~ 4.0% per annum (this is the typical rate in recent quarters) (India Post)

- No fixed term / maturity — you deposit, withdraw anytime (subject to rules).

- Minimum balance / deposit requirements are minimal (varies by branch).

- The interest earned is taxable (you declare it under income).

- There is an exemption: interest up to a certain small amount (often ₹10,000) from post office & bank savings accounts is exempt under Section 80TTA (for individuals).

Pros / Use cases

- Good for liquidity (you can access funds).

- Safe, government-guaranteed.

- Useful for storing emergency or working capital funds.

Limitations

- Low interest compared to other schemes.

- Because it’s taxable, net return may reduce.

Recurring Deposit (RD) / National Savings RD

What it is

You commit to depositing a fixed amount every month (say ₹100, ₹500, etc.) for a fixed tenure. This helps disciplined saving.

Key features

- Tenure: Usually 5 years for the post office RD / small savings RD. (

- You deposit equally each month.

- At maturity, you receive principal + interest.

- The interest rate is compounded quarterly.

- Current interest rate (for recent period) ~ 6.7% per annum (for RD) (source: small savings listing)

Pros

- Encourages regular savings for people who may not have lump sums.

- Safe.

- Good for goal-based saving (e.g. saving monthly for something 5 years ahead).

Limitations

- Less flexible — you must deposit monthly.

- Premature closure is possible in some schemes but often with penalties or different interest. Returns are moderate; interest is taxable.

Monthly Income Scheme (MIS) / Post Office Monthly Income Scheme (POMIS)

What it is

A scheme where you invest lump sum, and you receive fixed interest every month (monthly payout). Good for those wanting regular income, like retirees.

Key features

- Tenure: 5 years.

- Interest is paid monthly (i.e. you get a monthly “coupon” / income) at a fixed rate.

- After maturity, you get back the principal amount.

- Deposit (investment) limit: For single account ~ ₹9 lakhs; for joint ~ ₹15 lakhs.

- You can open joint or single accounts.

- You may be allowed to withdraw early after 1 year, but with penalty.

- Current interest rate: ~ 7.4 % p.a. (for recent quarter)

Pros / Use cases

- Good for people who want monthly income (e.g. retirees, pensioners).

- Predictable income.

- Safe / government backed.

Limitations

- Locked for 5 years unless you accept penalty.

- Because the interest is disbursed monthly, compounding is less beneficial compared to other schemes (you don’t keep interest accumulating).

- The effective yield is less if you reinvest the monthly payouts at lower rates.

- Interest is taxable in the year you receive it.

Time Deposit / Term Deposit (aka National Savings Time Deposit)

This is what we earlier called “Post Office FD / fixed deposit / term deposit”.

What it is

You invest a lump sum for a fixed duration (1, 2, 3, or 5 years). At maturity you get principal + interest (compounded quarterly).

Key features / interest rates (recently)

- Tenures: 1 year, 2 years, 3 years, 5 years.

- Minimum deposit needed: ₹1,000. No maximum limit.

- Interest is compounded quarterly, but paid annually / at maturity.

- For the 5-year term, deposit qualifies for deduction under Section 80C of Income Tax Act.

- Current interest rates (for recent quarter):

• 1 year → ~ 6.9 % p.a.

• 2 years → ~ 7.0 % p.a.

• 3 years → ~ 7.1 % p.a.

• 5 years → ~ 7.5 % p.a.

Pros / uses

- Good for people with lump sum money, who want safety and fixed returns.

- Particularly helpful if you don’t need liquidity for that tenure.

- 5-year option also gives tax deduction under 80C.

Limitations

- Locked in (unless you accept penalty for early withdrawal).

- For shorter tenures, returns are moderate compared with riskier instruments.

- Interest is taxable.

National Savings Certificate (NSC)

What it is

A government savings bond that you purchase at post offices. Popular among middle-class investors.

Key features

- Tenure: 5 years.

- Interest is compounded annually but payable at maturity.

- The investment qualifies for deduction under Section 80C.

- Current interest rate: ~ 7.7 % p.a. (for recent quarter)

- You can pledge NSC as collateral for loans.

- You can prematurely close in certain cases (e.g. death of holder) under rules.

Pros / uses

- Good option for middle to long-term safe investment.

- With tax benefit (80C) + decent returns, often used for tax planning.

- Predictable returns.

Limitations

- Locked 5 years (though early closure allowed only in limited cases).

- Interest is taxable (except the part allowed as 80C investment).

- Because interest is payable at maturity, you don’t get periodic income.

Public Provident Fund (PPF)

What it is

Long-term instrument for retirement / long-range savings, with tax advantage.

Key features

- Tenure: 15 years (initial lock-in)

- You can extend in blocks of 5 years after maturity.

- Partial withdrawals allowed from 7th year onward.

- Loans possible from 3rd year onward against the balance.

- Annual contributions (minimum ₹500, maximum ₹1,50,000 per year).

- Fully tax-free (the interest and maturity amount are exempt).

- The deposit qualifies for deduction under 80C.

- Current interest rate: ~ 7.1 % p.a. (recent)

Pros / use cases

- Excellent for long-term wealth accumulation / retirement savings.

- Tax-free returns + deduction under 80C = attractive.

- Low risk, government guarantee.

Limitations

- Long lock-in (15 years).

- Returns may be moderate compared to market instruments over long term.

- You need to regularly contribute annually (you can’t just invest a lump sum only once and forget).

Sukanya Samriddhi Yojana (SSY / SSA)

What it is

A scheme targeted at parents/guardians of girl children, intended to promote girls’ education and financial security.

Key features

- Only for girl children (account opened before she turns 10).

- Minimum deposit: ₹250; maximum per year: ₹1,50,000.

- Tenure: Account matures after 21 years from opening (or 21 years from deposit).

- You contribute for 15 years; after that no more deposits but account continues.

- Interest & maturity amount are tax-free.

- Interest is calculated yearly.

- Current interest rate: ~ 8.2 % p.a. (recent) (India Post)

Pros / uses

- Very attractive scheme for female child’s future (education, marriage).

- Tax benefits + high interest.

- Safe, government backed.

Limitations

- Restricted to girls only.

- Long horizon.

- Only 15 years of deposits allowed, then no more contributions.

Senior Citizens Savings Scheme (SCSS)

What it is

A scheme especially for senior citizens (age 60+, or some cases 55+ upon retirement) to get periodic income and safety.

Key features

- Tenure: 5 years. (nsiindia.gov.in)

- Interest is paid quarterly.

- Eligible deposit: maximum limit (there is a ceiling).

- The deposit qualifies under Section 80C. (nsiindia.gov.in)

- Interest is taxable.

- Current interest rate: ~ 8.2 % p.a. (recent) (India Post)

Pros / uses

- Good option for retirees wanting safe, decent returns with periodic income.

- The government backing gives reliability.

- Interest paid quarterly helps with regular income planning.

Limitations

- Locked 5 years unless special conditions.

- Returns can be lower after tax.

- Only those meeting age conditions can open.

Kisan Vikas Patra (KVP)

What it is

A certificate scheme where your invested amount “doubles” over a specified time, with fixed rate, designed to benefit small savers and encourage long-term deposit.

Key features

- There is a “doubling time” — your investment will double after a fixed duration (based on current interest rate) (Wikipedia)

- No maximum limit for investment.

- Can be purchased in multiples of ₹1,000.

- Maturity period depends on rate.

- It can be prematurely encashed (after certain time) under conditions.

- Current interest & doubling time: ~ 7.5 % p.a. (recent)

Pros / uses

- Good for those who want safe, guaranteed doubling over a medium time horizon.

- Simple to understand.

- Suitable for conservative savers.

Limitations

- The doubling time can be long (many years).

- You may not get frequent interest (interest is accumulated).

- The returns are lower than what equity or high risk instruments might offer in that horizon.

Mahila Samman Savings Certificate (2023)

What it is

A scheme introduced specifically for women / “Mahila” savings to encourage female financial inclusion.

Key features

- It is a kind of small savings product launched in 2023. (India Post)

- Offers a competitive interest rate, likely in the bracket similar to term deposits.

- Compounded quarterly. (India Post)

Because this is relatively new, details of maximum limit, full terms, etc., need verification from official sources.

Comparison Summary

Below is a comparative overview of these schemes in terms of tenure, interest, liquidity, tax advantages, and ideal target investor:

| Scheme | Tenure / Duration | Interest Behavior / Rate | Liquidity / Withdrawals | Tax Benefit | Ideal For / Use Case |

|---|---|---|---|---|---|

| Savings Account | No fixed term | ~4% p.a. | Withdraw anytime | Exemption of interest up to limit | Emergency fund, flexible use |

| Recurring Deposit | 5 years | ~6.7% p.a. (compounded) | Premature closure with penalty | No major tax benefit | Those who can save monthly |

| Monthly Income Scheme (MIS) | 5 years | ~7.4% p.a. (paid monthly) | Partial withdrawal after 1 year (penalty) | No tax benefit | Retirees wanting monthly income |

| Time Deposit (1 / 2 / 3 / 5 yrs) | 1 / 2 / 3 / 5 years | ~6.9%, 7.0%, 7.1%, 7.5% respectively | Early withdrawal with conditions / penalty | 5-yr option qualifies for 80C | Lump sum investors wanting safe returns |

| National Savings Certificate (NSC) | 5 years | ~7.7% p.a. | Withdraw only at maturity (with limited exceptions) | Yes (80C) | Medium-term safe investment |

| Public Provident Fund (PPF) | 15 years (extendable) | ~7.1% p.a. | Partial withdrawal from 7th year; loan facility | Yes; interest & maturity exempt | Long-term savers / retirement planning |

| Sukanya Samriddhi Account (SSY) | ~21 years (15 years of deposit) | ~8.2% p.a. | Some withdrawals for education/marriage | Yes; interest & maturity exempt | Savings for a girl child |

| Senior Citizen Savings Scheme (SCSS) | 5 years | ~8.2% p.a. (paid quarterly) | Partial withdrawal under rules | Yes (80C) | Senior citizens needing safe income |

| Kisan Vikas Patra (KVP) | Several years until doubling | ~7.5% p.a. (compounded) | Early withdrawal under rules | No (interest is taxable) | Medium-term doubling goal |

| Mahila Samman Savings Certificate | (Likely ~5 yrs) | Competitive (similar to term deposits) | Locked for tenure | TBD | Women savers |

Tips & Things to Watch

- Interest rate revisions

The Government of India revises interest rates of small savings schemes every quarter, based on yield of government securities, inflation, etc. So, new schemes get locked into rate at the time of deposit. - Lock-in periods & penalties

Many schemes enforce a lock-in or prevent full withdrawal before a certain period or with a penalty (e.g. MIS, RD, time deposit). - Tax implications

Not all schemes are tax-free. For example, interest on MIS, time deposit, KVP etc. is taxable. Some schemes (PPF, SSY) are fully exempt. Use tax planning accordingly. - Nomination and joint accounts

Many schemes allow joint accounts (for some schemes) or nomination so that in case of death, the nominee receives proceeds. - Transfer across post offices

Most schemes allow you to transfer the account from one post office to another (if you move residence). - Partial withdrawals / loans

Some schemes (PPF, NSC, etc.) allow partial withdrawal or loans under certain conditions. - Documentation & KYC

For new accounts, you need identity proof (Aadhaar, PAN, Voter ID, etc.), address proof, and in case of minor accounts, birth certificate. - Monitoring maturity

Some accounts, after maturity, may stop accruing interest (or freeze). Always plan to re-invest or withdraw timely.

Steps to apply for a Post Office FD online

Here is a step-by-step process according to available sources:

- Make sure you have an India Post Savings Account that is enabled for internet banking / e-banking.

- Go to the India Post eBanking / net banking portal.

- Log in with your registered User ID and password.

- Go to “Service Request” (or “General Services”) section.

- Select “New Request” or “Open Fixed Deposit / Time Deposit”.

- Fill in required details: deposit amount, tenure (1, 2, 3, or 5 years), nominee, etc.

- Confirm deposit from your linked savings account.

- Submit and complete the process.

If online is not possible (for your branch or location), you can always apply offline by visiting your nearest post office branch, filling the FD / time deposit application form, providing identity/address documents, and depositing the amount. (India First Life)

The Post Office Fixed Deposit scheme is an excellent risk-free savings option for people who value safety over high returns.

For a ₹2 lakh investment over 2 years, at the current interest rate of 7%, you can expect a maturity value of approximately ₹2,29,600. While the returns are modest compared to equity or mutual funds, the government guarantee makes it attractive, especially for conservative investors.

If you are investing with the objective of capital protection, guaranteed returns, and simple process, the Post Office FD scheme is worth considering.